1. Hybrid networking becomes a future trend, and TD-LTE and FDD-LTE are cooperative rather than competitive.

In overseas markets, the market share of operators will remain stable, as FDD-LTE is basically upgraded from WCDMA. However, the surge in demand for information traffic in the future will challenge the limited FDD-LTE spectrum, and the advantages of TD-LTE spectrum will remain attractive to operators. The complementary relationship between these two technologies allows them to coexist, which allows the TD-LTE network to occupy one-third of the market share in the future market, and will also benefit Chinese equipment suppliers.

Since WCDMA technology is widely adopted in the 3G field, most operators intend to enter the FDD-LTE market. FDD requires two symmetric spectrums to achieve up-and-down connectivity; however, tight spectrum resources lead to increased FDD costs, which requires operators to find solutions at a lower cost. In contrast, TDD does not require spectral symmetry and is therefore more cost effective. Many operators who do not have experience in TDD operation have accumulated a lot of TDD spectrum resources at low cost in bidding. Currently, they have both FDD and TDD spectrum; therefore, FDD/TDD hybrid networking can reduce construction costs and make full use of existing There is spectrum and at the same time provide faster service.

Compared to single-mode fiber, FDD-LTE and TD-LTE are similar in technology, so they can contribute to BBU, antenna feeder, GPS, transmission, network management and EPC solutions. Analysis of FDD/TDD network convergence shows that the cost only rises by less than 30%, but it will significantly increase the amount of data processing. In the LTE world, downstream connection transmission is more important for most data service users; operators will provide higher quality services through more spectrum resources while ensuring the flexibility of TDD technology.

FDD/TDD dual mode is the future trend of user equipment. The Polish operator Aero2 has started commercial operation of the FDD/TDD converged network since September 2011. Hi3G also launched commercial operation of 4G LTE network services in Stockholm, Gothenburg and Malmo, which is the world's first large-scale FDD/TDD dual-mode network commercial operation. Hi3G has only two 10MHz and 2.6GHz FDD bandwidths in Sweden and Denmark, which makes it difficult for LTE networks to provide competitive data processing. However, Hi3G also has a 50MHz FDD spectrum and a 25MHz spectrum in Sweden and Denmark, respectively. Therefore, FDD/TDDLTE hybrid networking will be the best choice, not only to provide high-speed data services, but also to provide spectrum resources more efficiently. China has also been promoting the development of FDD/TDD dual-mode networks. The dual-mode project is the testing focus of the TD-LTE Phase II pilot. China Mobile Hong Kong has launched the FDD/TDDLTE dual-mode network in Hong Kong, which is an important part of the hybrid networking pilot market.

Qualcomm is also supporting the convergence of TDD and FDD. Currently, the iPhone 5 uses a dual-mode chip. Qualcomm believes that FDD/TDD dual-mode equipment is the best premise for hybrid networking. FDD networks can provide larger area coverage and can be used as a hotspot and home base station in data processing and coverage, because TDD spectrum is relatively easy. Acquire, and a converged network can eliminate more interventions from different systems and reduce the complexity of network optimization. In addition, considering the development trend of mobile broadband, TDD will provide a “last mile†solution at a lower cost in India and other places (the privatization of Indian land leads to difficulties in cable and network construction). Considering the network structure, the core network is a public network and there is no difference in transmission. Leading base station vendors are able to share their platforms and fully leverage technology convergence.

2. Chinese equipment suppliers will usher in huge opportunities

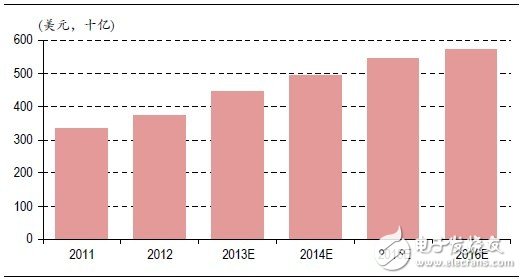

According to iSuppli, global mobile communications equipment revenue will increase to $570.9 billion by 2016. The LTE network will become a new revenue growth point for companies such as ZTE and Huawei. At the same time, the capital expenditure of wireless broadband will also drive the growth of capital expenditures for transmission and indoor coverage, which will benefit the transmission equipment suppliers such as FiberHome Communications and Optical Broadcasting Technology and indoor coverage provider Jingxin Communication.

Ericsson predicts that by the end of 2012, the number of mobile users worldwide will be 6.6 billion, and by 2018 it will reach 9.3 billion. In 2010, 2011 and 2012, mobile broadband users will be 600 million, 1 billion and 1.5 billion, respectively, and will reach 6.5 billion in 2018. WCDMA/HSPA services will cover half of the world's total population, and are expected to exceed 55% in 2013 and 85% in five years. The scale of development is comparable to today's GSM network. All WCDMA operators have delayed the construction of HSPA networks. In 2012, LTE network construction entered a growth period, and the LTE commercial network increased from 47 in 2011 to 147 in 2012. The GSA predicts that the number of LTE commercial networks will increase by 260 by the end of 2013. In addition, the number of LTE devices in 2012 will increase from 150% in 2011 to 560 units.

LTE has become the fastest growing telecommunications technology. It took three years for 3G's first pilot network to start commercialization, and HSPA took a year to commercialize, while LTE was less than nine months old. The operator has built 200 HSPA demonstration networks in two years, and LTE can reach the same scale in only 20 months. In addition, GSM has 30 million users in 51 months, WCDMA has been 45 months, and LTE only takes 31 months. In 2012, LTE services only covered 500 million users, and it is estimated that by 2017, the population will reach half of the global population. In 2012, LTE users played 5,000 games, and it is expected to reach 1.6 billion in 2018. The LTE market in the United States, Japan, and South Korea is growing rapidly, and its LTE users account for 95% of the total number of LTE users worldwide.

According to the technology development rules, the WCDMA network will be upgraded to an FDD-LTE network. It is speculated that WCDMA equipment suppliers will become FDD-LTE equipment suppliers, which will benefit traditional suppliers such as Ericsson. However, TD-LTE is a brand new network. In the Chinese market, some base stations can be upgraded directly from TD-SCDMA, but in overseas markets, the network must be rebuilt. As China Mobile has the largest TD-LTE network in the world, its suppliers ZTE and Huawei will remain in a dominant position while expanding their market share in the global telecommunications equipment sector.

Thanks to mobile broadband, the mobile device market will usher in a big development. According to iSuppli's survey, total OEM equipment revenue in mobile communications at the end of 2012 is expected to be $376 billion, up from $334 billion in 2011. In 2013, total revenue from mobile communications equipment will rise to $4.44 billion, as shown in the table below.

Figure 1. Global mobile communication device revenue forecast

Driven by mobile broadband, the compound annual growth rate for the five-year period to 2016 is expected to be 11%. HIS defines mobile communication device factory revenue as the revenue that manufacturers earn when they sell equipment to channels, that is, mobile communication devices such as smartphones and other mobile phones. This project also includes wireless infrastructure such as routers.

According to ABI research, global LTE wireless access network spending in 2013 was $12.3 billion, an increase of 82.4% year-on-year. Most countries in the world have joined this high-speed club. In addition to physical infrastructure, intangible LTE spectrum licenses also cost operators a lot of money. For example, the 4G mobile spectrum license acquired by French SFR last year only accounted for 38.9% of its capital expenditure. The fluctuations in capital expenditures of mobile operators are very obvious.

Moreover, Gartner predicts that the global RAN and EPC market will grow from US$4.1 billion in 2012 to US$21.1 billion in 2016. During the period, the LTE equipment market will grow at a compound annual growth rate of 58.5%, the fastest growing in the mobile infrastructure market.

Power Lan Transformers For Automotive Product,Ferrite Core Pluse Transformer,High Power Pulse Transformer,Pulse Transformer Vs Power Transformer

IHUA INDUSTRIES CO.,LTD. , https://www.ihua-inductor.com