(1) Government guidance + market means to solve the problem of persistent wind curtailment

Since last year, power grid enterprises and parties have adopted the unconventional means of government guidance (mandatory consumption) + market selection (transaction means) to solve the abandonment of wind in the "Three North" region.

The series of measures include: reducing pressure on thermal power, reducing system spare capacity, increasing coal power flexibility, cross-regional spot trading, coordinating eastern provinces, peaking auxiliary services, clean energy heating, UHV delivery, power generation The right transaction and other methods will focus on solving the problem of wind curtailment in the Three North Region, and will make room for new energy consumption.

In November 2017, the National Development and Reform Commission and the Energy Bureau issued the “Implementation Plan for Solving the Problem of Abandoning Water, Abandoning Wind and Abandoning Lightâ€, combining government guidance with market-based means, coordinating new energy supply and means market, and combining technological innovation with institutional reform. Improve the technical level of renewable energy power in all aspects of power supply, power grid and power consumption. Accelerate the pace of power market construction, improve the trading mechanism, auxiliary service mechanism and price mechanism to promote renewable energy power consumption, and continuously improve the market competitiveness of renewable energy power generation.

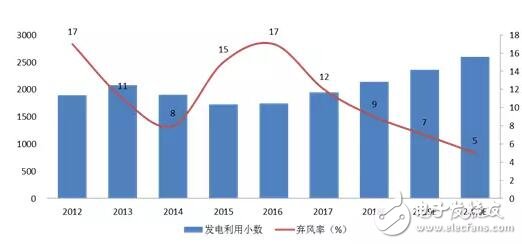

Chart 1 2016, 2017, the red six provinces abandoned the wind rate significantly improved

In April 2018, the National Energy Administration issued the "Clean Energy Absorption Action Plan (2018-2020) Consultation Draft", which clarified that 2018 has a light rejection rate of less than 5% and a wind curtailment rate of less than 12%; The rate is less than 5%, and the rate of abandoned wind is about 8%; in 2020, the light is less than 5%, and the wind is about 5%.

From the attitude and actions of the grid enterprises, the State Grid's second-quarter work conference proposed that the State Grid Corporation will conscientiously implement the spirit of the important instructions of the General Secretary of the internship, and make the development of new energy as a major political task, research and develop new energy sources in 2018. We will work out the work arrangements, put forward specific requirements from planning and construction, dispatching transactions, market mechanisms, and technological innovations, identify 22 key tasks, and comprehensively promote new energy consumption. Shu Yinbiao, chairman of the State Grid, said that he will continue to promote the development of clean energy, profoundly understand the arduousness of resolving the contradiction of "three abandonment", give full play to the role of the power grid, and accelerate the construction of a new generation of power systems.

Chart 2 Abandoned wind rate decreases year by year

According to the National Energy Administration, wind power increased by 3.94GW in the first quarter of 2018, an increase of 12% year-on-year. The national average wind curtailment rate dropped by 8 percentage points year-on-year to 8.5%. In the national grid area, the amount of abandoned wind and abandoned photoelectricity decreased by 53% and 32% respectively in the first quarter, and the wind and light rejection rate decreased by 11.2 and 6.1 percentage points respectively, which was the annual abandonment rate control. Set the foundation within 9%.

(II) The launch of new energy marketization transactions, expanding the space for industrial growth

There are two main forms of new energy participation in market-oriented transactions. One is to absorb energy as a distributed energy source and participate in regional power market transactions. The other is to cross-provincial cross-regional transactions to achieve greater adjustment and balance of energy structure.

1. Decentralized wind power is expected to test water market transactions, and the sale will improve the asset value.

At the end of March 2018, the National Energy Administration completed the collection of opinions on the "Distributed Power Generation Management Measures (Draft for Comment)". According to the National Energy Administration's pilot arrangement for market-based trading of distributed power generation, the distributed power generation market will be promoted at the latest on July 1 this year. The pilot of the transaction; the National Energy Administration requires the pilot area to measure the total size of distributed photovoltaic and decentralized wind power that can be accessed by the distribution network of 110 kV and below by 2020, and the scale of each year from 2018 to 2020 .

As a new energy supply main body, distributed power generation is taking advantage of its small scale, close to users, and a wide range of integrated energy services, enriching the form of market-based power trading. With the launch of the pilot of distributed power market transactions, it will be an innovative power trading model for distributed wind power and a price formation mechanism. It is expected to improve the economic benefits of decentralized wind power projects under the mode of integrating power generation and electricity sales.

Taking the Mengdong area as an example, the local area belongs to the category II resource area. The target price of the newly approved wind power project in 2018 is 0.45 yuan/kWh. If the market trades with the general industrial and commercial users, the transaction price is 0.78 yuan in the catalogue price. / kWh basis up and down 10%, the transaction price is 0.702 yuan / kWh, deducted network fees, government funds and additional, plus renewable energy subsidies, the market transaction price will still be higher than 0.45 yuan / Kilowatt hour benchmark price. Take the 10mw decentralized project in Mengdong area as an example. If the electricity price increases from 0.45 yuan/kWh to 0.702 yuan/kWh, the internal rate of return of the project will increase by 10 points under the utilization hours of 3000 hours. the above.

2. The new energy cross-regional market-oriented transaction started, expanding the wind power consumption space

In addition to administrative constraints, market-based trading instruments are an important channel for promoting clean energy consumption. In 2017, the power market trading volume in the national grid region was nearly 1 trillion kWh. The new energy cross-regional transaction is a new form of power market trading. With the expansion of the power market transaction scale, new energy grid-connected consumption will also be Benefit from this process.

At present, the Beijing Electric Power Trading Center of the State Grid and the relevant provincial power trading center actively adopt market-oriented trading mechanisms to implement 10 relevant market-oriented trading varieties that promote clean energy consumption. Among them, 7 trading varieties have been carried out in the normal way, including clean energy delivery transactions, clean energy and thermal power bundled delivery transactions, clean energy inter-provincial direct electricity transactions, new energy and electric heating / electric energy to replace direct transactions, cleaning Energy replaces conventional thermal power generation rights trading, clean energy replaces provincial coal-fired self-sufficient power plant transactions, and clean energy replacement transactions.

In addition to the normal trading varieties, Beijing Electric Power Trading Center and the National Electric Power Dispatching Control Center also explored and piloted three other market-oriented trading varieties, including pumping power storage and trough new energy trading, clean energy emergency consumption transactions and Cross-regional renewable energy spot trading.

In the first quarter, domestic new energy inter-provincial transactions continued to expand, and the State Grid accumulated a total of 18.894 billion kwh of cross-regional trading power of new energy, an increase of 65.22% year-on-year. Among them, the new energy cross-region spot transaction delivery power 2.869 billion kwh, an increase of 113%; new energy participation in the province's large users direct supply transaction power totaled 2.819 billion kwh, an increase of 89.55%.

(3) Clean up the non-technical cost of wind power and clear the road for the net price

The National Energy Administration issued the "Notice on Reducing the Burden of Enterprises in the Field of Renewable Energy" in April, and introduced a number of measures to reduce the burden on renewable energy and clean up the non-technical costs of wind power, photovoltaic and other clean energy industries, including local government violations. Wind power resource fees, violations require wind power investors to build factories, mandatory sharing of social welfare investments such as poverty alleviation undertaken by local governments, other investments bundled with scenery resources, and access fees charged by grid companies for violations.

The National Energy Administration requires local governments to return the resource fees collected for violations within one year, and encourage enterprises to participate in market transactions and promote the implementation of the quota system. The purpose of these measures is to calculate the enterprise electricity cost bills, accelerate the new energy parity online, and reduce financial pressure. Prepare for subsidies to retreat.

(4) The power generation transaction is accelerated, and fossil energy is a new energy space.

On May 11, the National Energy Administration issued the "Notice on Further Promoting the Work Related to Power Generation Trading". Under the background of the reform of power market reform and the promotion of clean energy consumption, the national energy management department accelerated the power generation trading, focusing on promoting Cross-regional power generation trading.

The so-called power generation transaction is a trading platform in which a power generation enterprise transfers its contracted electricity such as a base electricity contract and a priority power generation contract through a power market transaction, and transfers it to other power generation companies in a market-oriented manner such as bilateral negotiation, centralized bidding, and listing. . In principle, large-capacity, high-parameter, and environmentally-friendly units replace the low-efficiency, high-pollution thermal power units and shut down the generator sets to generate electricity. The clean energy generators such as hydropower, wind power, photovoltaic power generation, and nuclear power replace the low-efficiency and high-polluting thermal power generating units. Should not be reversed. In short, it is to replace fossil energy units with clean energy units.

What needs special attention is: At the Central Economic Work Conference held at the end of 2017, the national leaders clearly made important instructions for increasing the supply of clean electricity by power generation transactions, accelerating the construction of the electricity market, and substantially increasing the proportion of electricity market transactions. .

Standing at the current time, the connotation of power generation trading has evolved. In 2008, the former Electricity Regulatory Commission issued the Interim Measures for the Supervision of Power Generation Rights. At that time, the power generation transaction was mainly based on intra-provincial power grid transactions, and there were no specialized trading institutions such as Beijing Power Trading Center and Guangzhou Power Trading Center, and wind power, Photovoltaic has not yet been developed on a large scale, and clean energy trading is still dominated by hydropower and nuclear power, and power generation transactions are dominated by government mergers.

At present, the National Energy Administration emphasizes that no department (institution) may arbitrarily intervene in the trading of power generation rights, and may not make concessions and benefits, and may not set up pre-approval. In areas where hydropower, wind power, photovoltaic power generation, nuclear power and other clean energy consumption spaces are limited, encourage clean energy generator sets to replace each other's power generation, and further promote clean energy consumption by further promoting inter-provincial cross-regional power generation rights trading. Encourage coal-fired self-sufficient power plants that comply with national industrial policies and relevant regulations and have fair social responsibilities to participate in power generation trading through market-based methods, and replace power generation with clean energy.

The essence of power generation trading is the redistribution of power generation resources. The purpose is to replace coal-fired power with high-generation, clean energy and high-efficiency units to replace inefficient polluting units. From the perspective of energy structure adjustment and environmental protection, power generation rights trading is to reduce the power generation of coal-fired generating units and high-pollution units through economic compensation, encourage thermal power to make way for clean energy, and reduce internal energy consumption of power systems through cross-regional power generation transactions. Energy production and consumption structures increase the proportion of clean energy in the terminal.

Chart 3 A number of policies introduced to support the development of clean energy such as wind power

In 2018, it was the first year of decentralized wind power startup in China. In the first quarter, the National Energy Administration issued the Interim Measures for the Development and Construction of Decentralized Wind Power Projects, which clarified the decentralized wind power grid-connected standards, electricity prices and subsidy policies. The document was initiated by decentralized wind power projects. The order of the domestic wind power has entered a new stage of concentrated and decentralized development. The decentralized wind power approval and grid connection are expected to accelerate in the second half of the year.

Decentralized wind power is not an exotic product. “Local balance, near consumption†is the most important feature of decentralized wind power. The path of pilot, growth and expansion is completely opposite to that of large wind power bases. From the perspective of the development of the energy industry, decentralized wind power is the result of the development of domestic wind power to a certain scale, the need to re-establish a new order in the power system, the development of enterprises to seek new profit growth points, and the policy to guide the industry to establish a new equilibrium.

The Interim Measures for the Development and Construction of Decentralized Wind Power Projects has laid the foundation for the development of decentralized wind power.

(1) Decentralized wind power projects may choose one of the modes of “spontaneous use, surplus electricity access†or “full net access†when applying for approval. The project's self-use part of the electricity does not enjoy the subsidy of the National Renewable Energy Development Fund.

(2) The maximum voltage level of the distributed wind power grid connection is increased to 110KV. According to the previous documents, the distributed wind power access voltage level should be 35 kV and below; it is strictly forbidden to send power to 110 kV (66 kV) and above. The expansion of the access voltage level to 110kv means that the decentralized wind power project can absorb the important dividend of the scaled wind power installation scale policy in a wider range.

(3) Simplify the approval process, and try the “approval commitment system†for the first time. The National Energy Administration encourages local trial projects to approve project commitments and reduce the initial cost of the project. This is an important change in the process of decentralization and decentralization of the State Council and its subordinate ministries. The approval of the commitment system is a typical post-event supervision. The pre-approval to post-event supervision is a major advancement in the approval of domestic projects, and the government functions from project management to service transformation. The project development and management rights are handed over to the enterprise. Compared with the approval system, the process and time required for the approval of decentralized wind power projects will be greatly reduced.

At present, there are already distributed wind power projects in Henan, Hebei, Shanxi, Liaoning, Inner Mongolia, Hunan, Guizhou and Jiangsu. Among them, Hebei plans to develop distributed access to wind power of 4.3GW from 2018 to 2020, Henan's "13th Five-Year Plan" to build 2.1GW of distributed wind power, and Shanxi's "13th Five-Year" decentralized wind power project development and construction scale of 987.3MW . Guangxi, Guizhou and other provinces have already clearly planned to follow up the preparation of decentralized wind power construction plans. All major energy companies have begun to deploy in the field of decentralized wind power. In the second half of the year, decentralized wind power approval and grid connection are expected to accelerate.

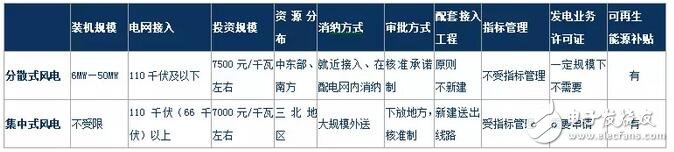

Figure 4 The main difference between distributed wind power and centralized wind power

In the second half of the year, wind power entered the peak season of equipment delivery, project construction and grid connection. At this stage, two indicators to measure the prosperity of the wind power industry, one is the indicator developed by the front end of the project, that is, the road strip; one indicator is the yield of the power station.

(1) The road strip is the industry wind vane

Although the national energy management department and the local government have banned the transaction of the roads, the road transaction is still the main channel for investors to obtain project resources (wind, light, etc.), and the price of the road is high and low and is positively related to the industry's prosperity. According to the information we obtained in the industry research, the current cost of the centralized wind power project in the high-quality areas of the north wind resources has risen sharply compared with last year. The price of some projects is about 0.6 yuan / watt.

The road strip is the wind vane of the industry's prosperity. In the past two years, the price changes of the road bills have reflected the continuous rise of the wind power industry. The increase in road tolls has pushed up the investment cost of the industry to a certain extent. Wind power developers are still willing to spend more on project resources. The driving force behind this is that the economic returns of wind power projects are greatly improved. Thanks to the improvement of the wind curtailment, the balance sheet of the stock wind power project was repaired, and the return on assets also rebounded from the bottom.

(2) Abandoning wind power cuts and improving the value of wind power assets

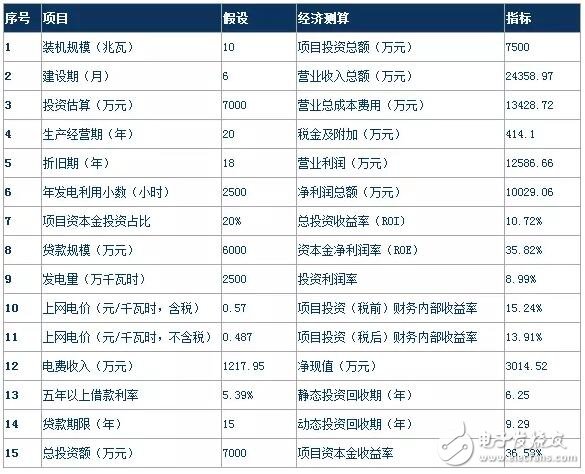

According to our research and calculation, the internal rate of return of some wind power projects with high quality of wind resources is around 15%. Take a 21MW decentralized wind power project in Inner Mongolia as an example. The project is connected to the grid for more than one year. The pre-conversion power generation utilization fraction is 3,300-3,400 hours, which is more than 1452 hours (the national average of 1948 hours). According to financial data analysis, the gross profit margin of power generation projects in 2017 was 75%, the net interest rate was as high as 59%, and the return on net assets was 38%.

Chart 5 Economic indicators of a 21MW distributed wind power project in Inner Mongolia

Driven by economic returns, stock developers are willing to increase the size of capital expenditures. New investment entities are beginning to flood into the wind power industry and are known as “barbarians at the doorâ€. These "barbarians" have both financial investors and investment entities that have turned from traditional industries such as oil and gas, as well as followers who are eager to follow. Their arrival will change the ecology of the wind power industry.

Chart 6 New players in the wind power industry are increasing

For the purpose of measuring the economics of the wind power project, we take a 10MW wind power project in the four resource zones as a sample, build a profit statement model and cash flow model for the 20-year operation period, and measure the project cost, revenue, and internal rate of return. Financial indicators such as capital yield and return on equity.

Under 2,500 hours of utilization hours, 0.57 yuan / kWh (including tax) on-grid tariffs, wind power projects have a leading market return on investment, stable cash flow and profit return. The economical calculation of the 10MW wind power project is as follows: the accumulated operating profit of the project is 126,586,600 yuan, the net profit is 100,290,600 yuan, the project's net assets return rate is 35.82%, and the project investment (after tax) financial internal rate of return is 13.91%. %; the net present value of the project investment is 30.145 million yuan, the static investment recovery period is 6.25 years, and the project capital return rate is 36.58%.

Chart 7 10mw wind power project economic calculation: leading return and cash flow

(3) Wind level price online stress test

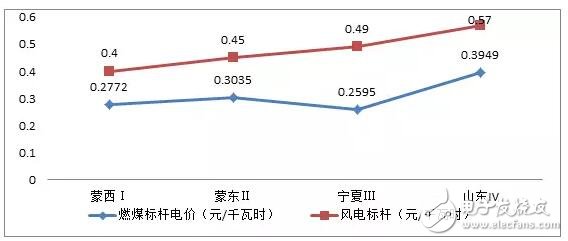

Although the price of wind power poles is continuously lowered, it is still at a relatively high level compared with the price of coal-fired benchmarks. We selected four representative provinces of wind power resource areas to compare with local coal-fired electricity prices. In the first-class resource area, Mengxi wind power and coal-fired power benchmarks were the smallest, followed by Mengdong, the second-class resource area.

Figure 8 The price difference between wind power poles and average coal-fired electricity prices in four resource zones in 2018

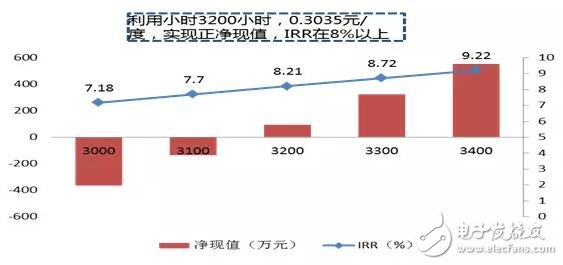

Let's take the Mengdong area as an example. If the price of wind power and coal is the same, take the on-grid price for the coal-fired benchmark price of 0.3035 yuan / kWh, and take the project cost of 6,500 yuan / kW. The economic calculation model shows that when the power generation utilization hours are 3000, 3100 hours, the project net present value is negative, the project does not have the economic conditions for development; when the power generation utilization hours are 3200 hours, the net present value is positive, the internal income The rate is above 8%; 3300-3400 hours, the internal income level continues to rise. It can be seen that increasing the number of hours of power generation utilization is an important prerequisite for the price of the wind.

Figure 9 Change in yield of Mengdong Wind Power Project under affordable Internet conditions

In September 2017, the National Energy Administration announced the first batch of 13 wind level Internet projects. The wind power of 707,000 kilowatts in Hebei, Heilongjiang, Gansu, Ningxia and Xinjiang became the first projects of affordable Internet access. According to the promise, the demonstration project will not be restricted by the provincial annual scale index; the on-grid electricity price is the local coal-fired benchmark on-grid price, no subsidy, no green certificate; all parties will promote unlimited electricity; the project will be completed and the wind power company will sign a purchase and sale agreement.

The National Energy Administration tested the two bottom lines through demonstration projects. One is the bottom line for wind power operators' profitability, and the other is the bottom line for the power grid to fully absorb new energy. We expect that in the second half of the year, under the pattern of continuous improvement of wind power abandonment, or demonstration projects will be the first to achieve parity online.

Fourth, wind power growth is driven by policy to economic drive, and the third round of growth can be expectedLooking back on the 15 years of China's wind power development, with 2007 as the starting point, the wind power industry has gone through two growth cycles, and 2018 is the beginning of a new cycle. The first and second rounds of growth began with the promulgation and implementation of the Renewable Energy Law, the establishment and adjustment of wind power benchmarking prices, and the medium and long-term development planning of clean energy. Top-down policy support is the driving force for wind power development.

As before, unlike the first and second rounds of growth cycle, the driving force for driving wind power into the third growth cycle is mainly from the improvement of the industry's own economic returns and the return of asset value, superimposed industrial policy, high density, sustained support, wind power It is expected to enter a new stage of growth.

Figure 10 Wind power industry development 15 years through two complete growth cycles

From the distribution of new installed capacity over the years, the market share of the top five wind turbine manufacturers in China has been continuously improved. With the expansion of comprehensive energy services such as cost advantages, financing, operation and maintenance services, the market share of wind power equipment leading companies is expected to continue to increase, and wind power equipment field 2 The reshuffle will also occur during the growth of wind power, and the advantages of leading companies will become more apparent. Benefiting from the new growth drive of the wind power industry, the demand for wind turbine equipment will be heavy.

The risk factors facing the industry include: the growth of wind power installed capacity is not as expected, the decline in wind turbine prices has led to a sharp fall in gross profit, and the sharp drop in wind power on-grid tariffs.

Stylus Pen Tip,Stylus Pencil Tip,Carbon Fiber Pen Tip,Carbon Fiber Stylus Pen Tip

Shenzhen Ruidian Technology CO., Ltd , https://www.wisonens.com